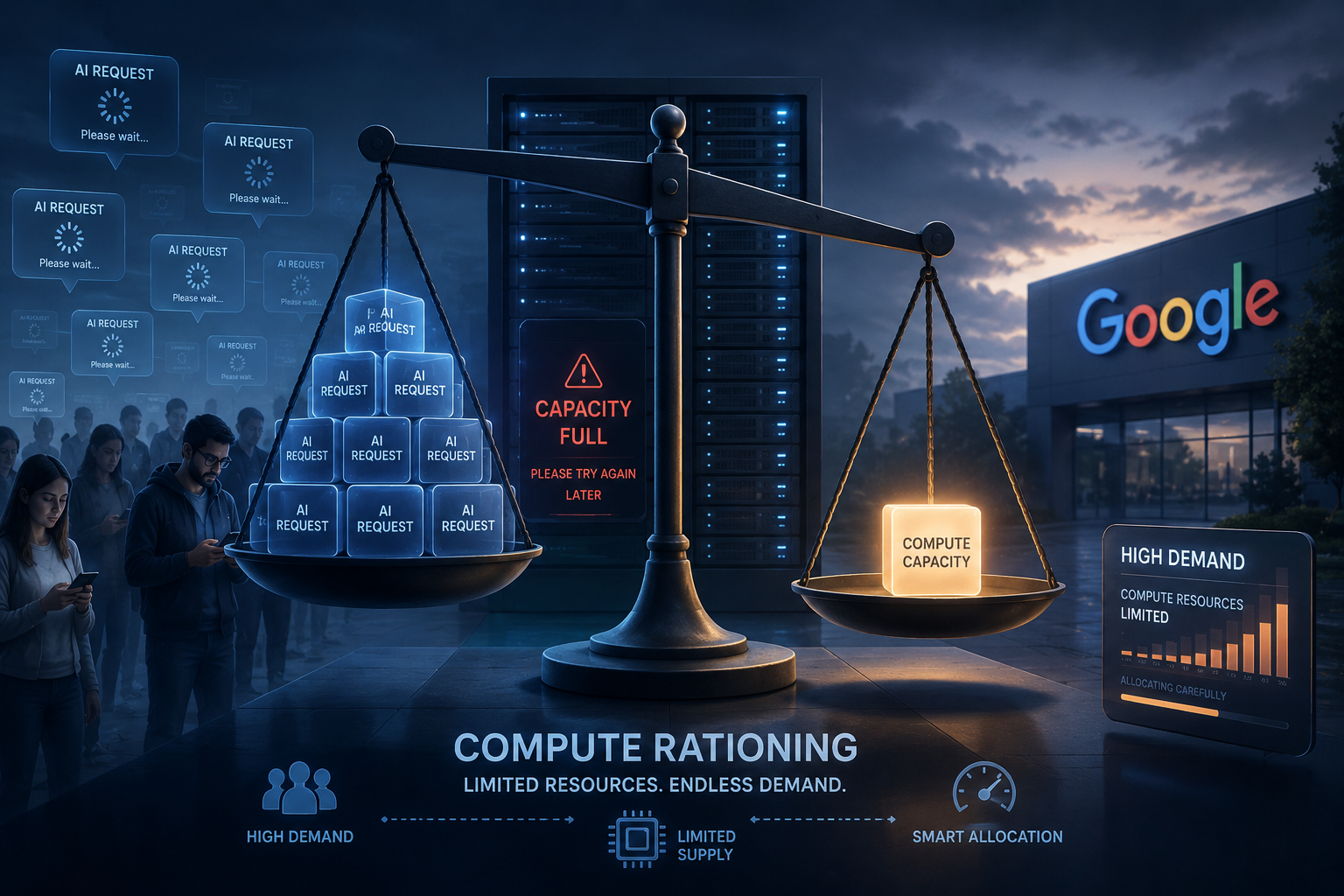

Here’s the thing: compute rationing isn’t some abstract policy concept. It’s what happens when even Google — a company that builds its own chips — can’t get enough GPUs and TPUs to serve every customer knocking on its door. And that’s exactly where we are right now.

The AI boom has genuinely outpaced the infrastructure meant to support it. I’ve been covering this industry for a decade, and I don’t say “structural crisis” lightly. But cloud providers turning away paying customers, governments drafting licensing frameworks, startups scrambling for scraps of GPU time — that’s not a hiccup. That’s a reckoning.

Why Cloud Providers Are Rationing GPU and TPU Access

The HBM Memory Bottleneck and Hardware Supply Chain Crisis

Cost-Per-Inference Trends and Real-World Rationing Examples

Government Licensing and Model Distillation as Rational Responses to Scarcity

Photonic Computing, Edge AI, and the Path Beyond Silicon Bottlenecks

Why Cloud Providers Are Rationing GPU and TPU Access

The math is brutally simple.

AI training and inference need specialized hardware — specifically GPUs and TPUs. But global chip production can’t keep pace with demand that’s growing faster than any supply chain can handle. NVIDIA controls roughly 80% of the AI accelerator market, and their H100 and newer B200 chips are the gold standard for training large language models. However, manufacturing them requires advanced packaging and scarce High Bandwidth Memory (HBM). Every major cloud provider — Google, Amazon, Microsoft — is elbowing for the same limited pool of supply.

So what does rationing actually look like in practice?

- Google Cloud has implemented waitlists for TPU v5p access, with some customers waiting months for an allocation

- Microsoft Azure has restricted GPU availability in certain regions, prioritizing enterprise contracts

- Amazon Web Services has introduced capacity reservations requiring long-term commitments

- Oracle Cloud reportedly signed a $2 billion deal with NVIDIA just to lock in chip supply

This surprised me when I first dug into it: compute rationing means when even Google doesn’t get preferential treatment from its own supply chain. Google designs TPUs internally — and still hits a wall. The bottleneck is foundry capacity at TSMC (Taiwan Semiconductor Manufacturing Company), where advanced nodes are oversubscribed. Every chip Google builds is a chip someone else doesn’t get. Consequently, smaller cloud providers like CoreWeave and Lambda Labs have raised billions specifically to secure hardware ahead of demand.

Scarcity has turned AI compute into something resembling a commodities market. With prices to match.

Meanwhile, the rationing isn’t always visible. Sometimes it shows up as:

- Degraded model quality — companies quietly swap in smaller models to save compute

- Rate limiting — API providers throttle requests during peak hours

- Geographic restrictions — certain GPU types simply unavailable in specific regions

- Longer training cycles — researchers queuing for cluster access that never quite arrives

I’ve talked to founders who’ve waited three months for GPU allocation they were promised in two weeks. That’s not an edge case anymore — it’s the norm. One founder building a medical-imaging tool told me she had to delay a clinical pilot by six weeks because the GPU cluster she’d budgeted for simply wasn’t available when her team was ready to train. She ended up redesigning a preprocessing pipeline to cut compute requirements by 30% — not because it was the right engineering decision at that moment, but because it was the only way to move forward with what she could actually get.

That kind of forced improvisation is becoming a standard part of the AI development process. It’s worth building it into your planning assumptions now.

The HBM Memory Bottleneck and Hardware Supply Chain Crisis

You genuinely can’t understand compute rationing without understanding the memory wall. Modern AI accelerators are only as fast as the memory feeding them data. That memory is HBM — High Bandwidth Memory — and it’s in desperately short supply right now.

HBM stacks memory chips vertically using through-silicon vias (TSVs). It’s an engineering feat that delivers enormous bandwidth. But it’s also incredibly difficult to make — only three companies do it at scale: SK Hynix, Samsung, and Micron. SK Hynix currently dominates, supplying most of NVIDIA’s HBM3E modules. That concentration of supply in one company is a fragility the whole industry is glossing over.

Here’s why the bottleneck isn’t going away soon:

1. Yield rates for HBM3E are low — stacking 8 or 12 DRAM dies with TSVs produces significant waste

2. Each NVIDIA H100 needs 80GB of HBM — the B200 pushes that to 192GB

3. New fabs take 2–3 years to build — meaningful capacity additions won’t land until 2026–2027

4. Testing infrastructure is limited — HBM requires specialized testing equipment that’s also backordered

To put the yield problem in concrete terms: if a production run of HBM3E stacks produces 30% defective units, the effective output of that run is 30% lower than the nameplate capacity suggests. Multiply that across every GPU waiting for memory, and you start to see why chip shipment forecasts keep slipping. It’s not that manufacturers aren’t trying — it’s that the physics of stacking a dozen ultra-thin dies with microscopic copper vias is genuinely unforgiving.

Notably, the Synaptics acquisition of Onsemi’s connectivity assets signals consolidation happening across the broader chip ecosystem. Companies are repositioning to capture value in AI-adjacent hardware — because everyone can see where the chokepoints are. Additionally, packaging firms like ASE Technology are expanding capacity for the advanced packaging HBM demands.

Compute rationing means when even Google doesn’t have enough memory chips to build all the TPUs it wants to build. Google’s TPU v5p uses HBM2E, and the next generation will need HBM3E — putting Google in direct competition with NVIDIA, AMD, and everyone else for the same constrained supply.

The real kicker? HBM prices have roughly doubled since 2023. Furthermore, that cost flows directly into AI inference pricing. Every chatbot response, every image you generate, every code completion — it all carries a hardware cost that’s rising, not falling. The “AI is getting cheaper” narrative is true at the per-token level, but total infrastructure spend keeps climbing because demand is growing faster than efficiency gains.

One practical implication that often gets overlooked: if you’re building a product that relies heavily on large-context inference — processing long documents, extended conversations, or large codebases — your memory costs are disproportionately high. Long-context workloads consume HBM at a rate that scales with context length, not just model size. Designing your application to chunk inputs intelligently or cache intermediate results can meaningfully reduce your memory footprint and, by extension, your exposure to HBM-driven price increases.

Cost-Per-Inference Trends and Real-World Rationing Examples

What does compute scarcity actually mean for costs? The numbers tell a clear story.

| Metric | Early 2023 | Late 2024 | Projected 2026 |

|---|---|---|---|

| Cost per million tokens (GPT-4 class) | $30–60 | $3–10 | $0.50–2.00 |

| GPU rental (H100/hr) | $3.50–4.00 | $2.00–3.50 | $1.00–2.00 |

| Waitlist for cloud GPUs | Days | Weeks–Months | Expected to ease |

| HBM cost per GB | ~$10 | ~$18–20 | ~$12–15 |

Importantly, per-token costs are genuinely falling — software optimizations are doing real work here. But here’s the thing: absolute demand for compute is growing faster than those savings. Companies are running more inference, not less. So total spending keeps climbing even as unit costs drop. It’s a treadmill.

Real-world rationing examples paint a vivid picture. Anthropic reportedly struggled to secure enough compute for Claude’s initial scaling push. Stability AI’s financial difficulties were partly driven by runaway GPU costs. Even Meta’s Llama models required massive internal GPU clusters that took priority over other Meta projects — which tells you something about how intense the internal competition for resources gets at scale.

Consider what that internal competition looks like in practice. At a company like Meta, a product team building a recommendation-system feature might find its GPU allocation cut mid-quarter because a foundation-model training run needs the headroom. The product team doesn’t lose access permanently — but they lose weeks, which in a competitive product cycle can mean losing ground to a rival. That’s compute rationing operating inside a single organization, not just between companies.

Compute rationing means when even Google doesn’t have infinite resources, smaller players face existential pressure. A startup training a foundation model might need 10,000–30,000 GPUs for months. At current rental rates, that’s $50–150 million in compute alone — assuming you can even get the GPUs. I’ve spoken with founders who’ve had to redesign their models around what hardware they could actually obtain. That’s a profound constraint on innovation.

Consequently, the industry is developing creative workarounds — model distillation, quantization, and architectural improvements all aim to squeeze more out of less hardware. They’re not optional nice-to-haves anymore. They’re survival strategies. A useful rule of thumb: before committing to a training run, benchmark your model at two or three smaller scales to validate that the architecture actually improves with more compute. Discovering a fundamental design flaw after you’ve burned through a $2 million cluster reservation is a mistake you only make once.

Government Licensing and Model Distillation as Rational Responses to Scarcity

When a critical resource becomes scarce, governments get involved. That’s not cynicism — it’s just history.

The gated access approach involves government licensing of compute resources. The U.S. Department of Commerce has already put export controls on advanced AI chips, restricting NVIDIA’s ability to sell H100s and A100s to certain countries. Essentially, the U.S. government is rationing compute at a geopolitical level. Similarly, the EU is developing its own framework — the EU AI Act includes provisions that could affect compute allocation for high-risk AI systems. Governments have figured out that controlling compute means controlling AI development.

The geopolitical dimension has a concrete downstream effect on enterprise planning. A company headquartered in the EU that relies on U.S.-based cloud GPU capacity for a high-risk AI application — say, a medical-diagnosis tool — may find itself navigating both U.S. export-control compliance and EU AI Act compute-reporting requirements simultaneously. That’s not a hypothetical; legal teams at several large European enterprises are already working through exactly this scenario. If your product roadmap involves regulated AI applications and cross-border cloud infrastructure, building in a compliance review at the architecture stage is significantly cheaper than retrofitting it later.

But there’s a flip side worth paying attention to.

Model distillation has emerged as one of the most rational responses to scarcity. Distillation trains a smaller “student” model to mimic a larger “teacher” model. You end up with a compact model that captures most of the teacher’s capability at a fraction of the compute cost. I’ve tested distilled models against their full-size counterparts — the quality gap is often smaller than you’d expect.

Why distillation matters specifically for rationing:

- A distilled model might need 10–100x less compute for inference

- Training the student is cheaper than training a new large model from scratch

- Edge deployment becomes viable, reducing cloud compute demand

- Companies can serve more users with the same hardware budget

Nevertheless, distillation raises thorny legal questions. OpenAI’s terms of service prohibit using its outputs to train competing models, and Google has similar restrictions. When companies distill from competitors’ models, it’s sometimes called “stealing efficiency.” The legal picture is still evolving — and honestly, it’s going to get messy before it gets cleaner.

There’s also a technical tradeoff that practitioners often underestimate: a distilled model inherits the teacher’s failure modes along with its strengths. If the teacher model produces confident but wrong answers on a particular class of inputs, the student frequently learns to replicate that behavior. Before deploying a distilled model in production, it’s worth running a targeted evaluation on the edge cases where the teacher is known to struggle — not just on the benchmarks where it shines.

Compute rationing means when even Google doesn’t have spare capacity, efficiency becomes a genuine competitive weapon. Companies that master distillation, pruning, and quantization gain an enormous structural advantage. Moreover, they reduce dependency on scarce GPU supply — which is worth a lot when your competitor is stuck on a three-month waitlist.

Specifically, techniques like GPTQ quantization can reduce model size by 4x with minimal quality loss. Mixed-precision training cuts memory requirements significantly. These aren’t theoretical — they’re deployed in production at companies you use every day.

Photonic Computing, Edge AI, and the Path Beyond Silicon Bottlenecks

Silicon-based computing has physical limits. Although engineers keep pushing those limits with impressive creativity, alternative approaches are attracting serious money and serious talent.

Photonic computing — using light instead of electrons — could fundamentally change the compute equation. And no, this isn’t vaporware.

Photonic processors offer several real advantages:

- Light travels faster than electrons and generates dramatically less heat

- Optical interconnects move data between chips at higher bandwidth

- Matrix multiplications (the core operation in AI) map naturally to optical interference patterns

- Power consumption could drop by 10–100x for certain workloads

Companies like Lightmatter and Luminous Computing are building photonic AI accelerators. They’re not ready to replace GPUs yet — I want to be clear about that. However, they represent a credible path toward breaking the compute bottleneck within 5–10 years. The physics is sound. The engineering is hard. There’s a difference.

One important caveat for anyone tracking this space: photonic computing excels at the dense matrix multiplications that dominate transformer inference, but it handles irregular, sparse workloads less gracefully. That means photonic accelerators are likely to emerge first in narrow, high-volume inference applications — think large-scale recommendation engines or image-classification pipelines — rather than as general-purpose replacements for GPUs. The path to broad adoption runs through specialized use cases first.

Edge AI offers more immediate relief, and this is where I’d focus attention right now. Instead of routing every inference request to the cloud, edge devices can run smaller models locally. Apple’s on-device AI processing, Qualcomm’s Snapdragon X Elite chips, and Google’s Tensor processors are all pushing compute to the edge — and the capability is improving faster than most people realize.

Compute rationing means when even Google doesn’t have enough cloud capacity, edge computing becomes strategically important. Every inference handled on a phone or laptop is one fewer request hammering the data center. Furthermore, edge processing reduces latency and improves privacy — two benefits that matter to users independent of any supply crunch.

A practical example: a customer-service application that handles initial intent classification on-device before routing only complex queries to a cloud model can cut its cloud inference volume by 40–60% in typical deployments. The on-device model handles the easy cases — greetings, simple FAQs, obvious routing decisions — and the cloud model handles the nuanced ones. That split architecture is already in production at several large consumer apps, and the economics are compelling even before you factor in the availability benefits.

The timeline for meaningful relief looks roughly like this:

1. 2025 — New GPU architectures (NVIDIA Blackwell, AMD MI350) increase per-chip performance by 2–4x

2. 2025–2026 — HBM production capacity expands as new fabs come online

3. 2026–2027 — Next-generation packaging technologies improve chip yields

4. 2027–2030 — Photonic and other alternative computing approaches reach commercial viability

5. 2028+ — Supply-demand balance potentially normalizes

Alternatively — and I think this is genuinely underappreciated — demand could keep outpacing supply. If AI agents, autonomous vehicles, and scientific computing all scale at the same time, the bottleneck could persist well into the 2030s. That’s not catastrophizing. That’s reading the demand curves honestly.

Conclusion

Bottom line: compute rationing is real, it’s structural, and it’s touching every corner of the tech industry. From HBM memory shortages to government export controls, the scarcity of AI compute is driving fundamental changes in how we build, deploy, and regulate artificial intelligence. I’ve watched a lot of tech cycles over the past decade — this one has a different weight to it.

The crisis isn’t permanent. Hardware improvements, software optimizations, and alternative computing approaches will gradually ease the pressure. However, relief won’t arrive overnight — and moreover, it won’t arrive uniformly. Some players will be squeezed far longer than others. Companies and developers need strategies for handling scarcity today, not 2027.

Actionable next steps worth considering:

- Optimize your models aggressively — use quantization, pruning, and distillation to cut compute requirements before you need to

- Diversify your cloud providers — don’t rely on a single vendor for GPU access; that’s a fragility you can actually fix

- Explore edge deployment — run inference locally wherever the use case allows

- Lock in capacity early — sign reserved instance agreements if you need guaranteed access; the spot market is brutal right now

- Monitor the policy picture — government licensing frameworks will affect compute availability in ways that are hard to predict

- Check alternative hardware — AMD, Intel Gaudi, and custom ASICs may offer better availability than NVIDIA, notably in certain regions

Compute rationing means when even Google doesn’t get everything it needs. Specifically, that reality should be baked into your AI strategy for the next several years — not treated as a temporary inconvenience you can plan around.

FAQ

What does compute rationing actually mean for everyday AI users?

For most consumers, compute rationing shows up as slower response times, rate limits on AI tools, and degraded model quality during peak hours. You might notice your AI assistant taking longer to respond, or you might hit usage caps you didn’t encounter six months ago. Importantly, companies manage scarcity by throttling access rather than turning users away entirely — so the experience degrades gradually in ways that are easy to miss until you compare it to how things worked before.

Why can’t Google simply build more TPUs to solve the shortage?

Google designs its own TPUs, but TSMC builds them — and TSMC’s advanced nodes are oversubscribed. Additionally, compute rationing means when even Google doesn’t control its entire supply chain. HBM memory, advanced packaging, and testing equipment all face independent bottlenecks that can’t be solved by throwing money at one part of the problem. Building more fabs takes years and billions of dollars. Consequently, the timeline for relief is measured in years, not quarters.

How does the HBM memory shortage affect AI chip production?

HBM (High Bandwidth Memory) is essential for modern AI accelerators. Each GPU or TPU needs large amounts of HBM to feed data to processing cores fast enough to be useful. Only three companies — SK Hynix, Samsung, and Micron — produce HBM at scale. Consequently, HBM supply directly limits how many AI chips can be assembled, regardless of how many processor dies are available. It’s a genuine single point of failure in the global AI supply chain.

Keep reading

Here are the latest posts from the blog.

When MCP supply chain attacks first showed how tool integrations can compromise entire AI systems, the implications were genuinely staggering. The Model Context Protocol (MCP…

AeroVironment’s revenue jumping to roughly $2.8 billion isn’t just an earnings beat. It’s a signal about how militaries actually fight wars now — and, more importantly, how t…

Six months of rapid releases, gated rollouts, and shifting pricing have fundamentally reshaped who can access what in the AI market. I’ve been tracking these changes in real…