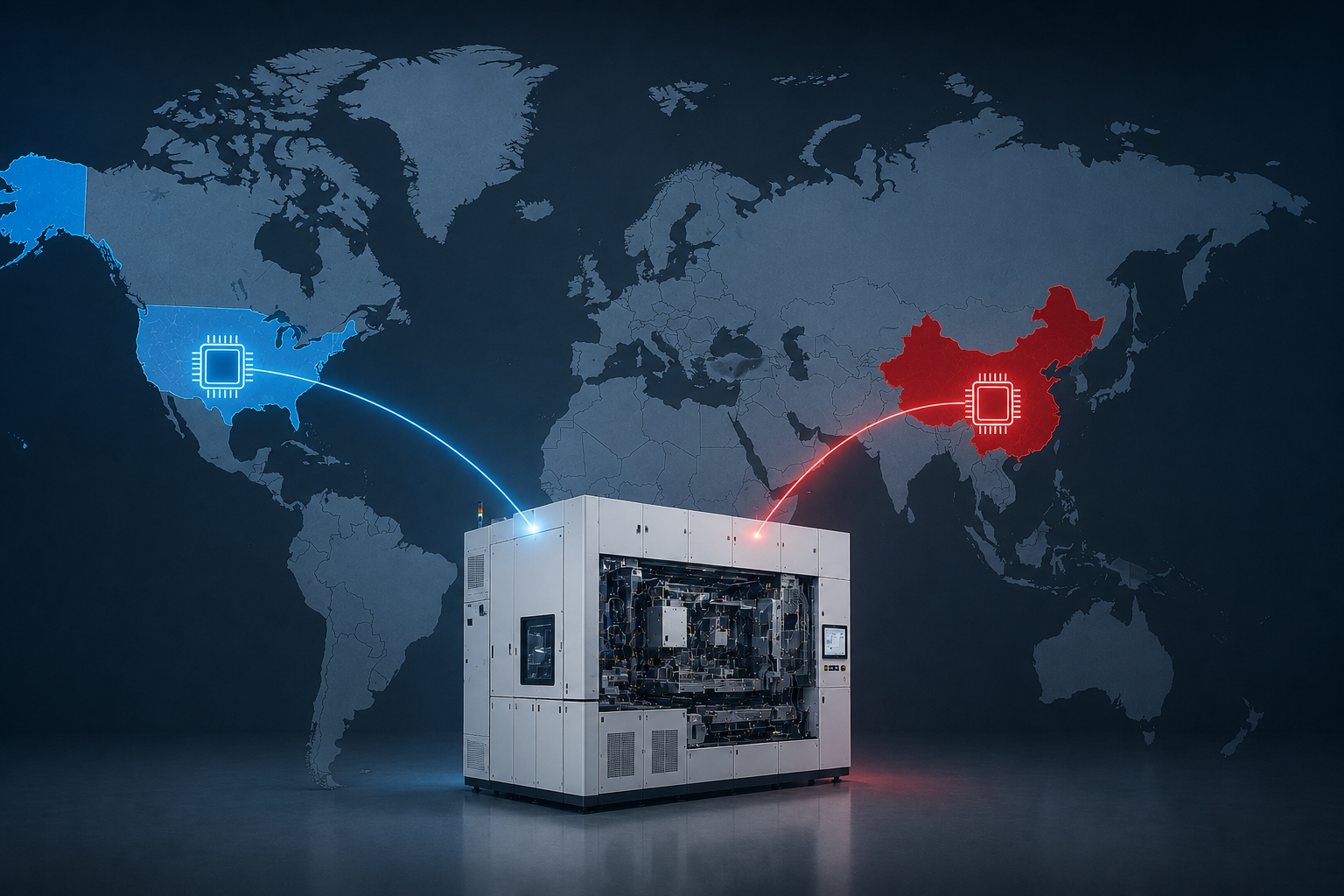

If you’d told me ten years ago that a Dutch optics company and a Taiwanese foundry would become the most strategically important businesses on Earth, I would’ve laughed. But here we are. Export controls explained how a handful of machines became the centerpiece of global AI policy isn’t hyperbole — it’s just where we ended up.

Governments aren’t losing sleep over AI models anymore. They’re focused on something far harder to copy, smuggle, or replicate: the physical hardware that makes AI possible. You can’t download a chip fab. You can’t jailbreak a lithography machine. That’s precisely why chips have become the new chokepoint — and why this matters to anyone paying attention to tech policy.

Why Hardware Is the Real Bottleneck

The Chokepoint Strategy: Controlling AI’s Supply Chain

How a Handful of Machines Became Geopolitical Leverage

The Nuclear Analogy: Chips Are the New Centrifuges

Real-World Impacts and Enforcement Challenges

Why Hardware Is the Real Bottleneck

Software gets all the headlines. ChatGPT, Claude, Gemini — these are the names people recognize. However, every single one of those models runs on specialized hardware. Specifically, they need advanced GPUs and custom AI accelerators built on the latest semiconductor nodes. No hardware, no frontier AI. It really is that simple.

Here’s the thing: AI models can be copied in seconds. A trained neural network is just a file. Someone can leak it, reverse-engineer it, or rebuild it from a research paper. Consequently, trying to control AI at the software layer is like trying to hold water in a net — it’s a losing game, and the people writing these policies know it.

Chips are fundamentally different. Building a state-of-the-art AI chip requires:

- Extreme ultraviolet (EUV) lithography machines costing over $150 million each

- Cleanroom facilities spanning hundreds of thousands of square feet

- Supply chains involving dozens of countries

- Engineering expertise built up over decades

- Chemical precursors and specialized materials from a handful of suppliers

Therefore, when we talk about export controls explained how a handful of machines became strategic assets, we’re really talking about physics. You can’t virtualize a fab. You can’t 3D-print an EUV light source. The physical world imposes limits that the digital world simply doesn’t — and that asymmetry is the whole ballgame.

Moreover, only one company on Earth — ASML in the Netherlands — makes the most advanced lithography machines. That single-supplier bottleneck gives export controls extraordinary leverage. Block ASML shipments, and you’ve effectively blocked a nation’s ability to manufacture leading-edge chips. One company. One product line. That’s it.

The Chokepoint Strategy: Controlling AI’s Supply Chain

The United States didn’t stumble into this strategy. It was deliberate. Starting in October 2022, the Bureau of Industry and Security (BIS) at the U.S. Department of Commerce rolled out sweeping restrictions on semiconductor exports to China. These rules targeted three layers simultaneously — and the coordination required was genuinely unprecedented.

Layer 1: Finished chips. NVIDIA’s A100 and H100 GPUs were restricted from export to Chinese entities. These chips power the largest AI training runs in the world. Notably, NVIDIA initially designed a downgraded chip — the A800 — to comply with the rules. BIS then closed that loophole too. The cat-and-mouse started almost immediately, which tells you something.

Layer 2: Chip-making equipment. The U.S. pressured the Netherlands and Japan to restrict exports of advanced lithography and etching tools. This wasn’t just about American companies — it required real diplomatic heavy lifting across allied governments. Getting allies to voluntarily hurt their own exporters is harder than it sounds.

Layer 3: Talent and knowledge. U.S. persons — including green card holders — were barred from supporting advanced chip development at certain Chinese facilities. This “human capital” restriction was unprecedented in scope. If you work in semiconductors and hold a U.S. green card, this layer affects you directly.

Additionally, the January 2025 “AI Diffusion Rule” created a tiered system. Countries were sorted into three groups based on their strategic alignment:

| Tier | Description | Access Level | Examples |

|---|---|---|---|

| Tier 1 | Close allies and partners | Largely unrestricted chip access | UK, Japan, Australia, Netherlands |

| Tier 2 | Most other countries | Capped chip purchases with licensing | India, Brazil, Saudi Arabia |

| Tier 3 | Arms-embargoed or adversary nations | Severely restricted or banned | China, Russia, Iran, North Korea |

This tiered framework shows export controls explained how a handful of machines became instruments of alliance management. Chip access isn’t just about technology anymore — it’s about geopolitical loyalty. That’s a significant shift from how the semiconductor industry operated even five years ago.

Furthermore, the restrictions extend beyond the chips themselves. BIS controls advanced packaging technologies, high-bandwidth memory (HBM), and even certain electronic design automation (EDA) software tools. The goal is complete coverage of the entire AI hardware stack. If it touches frontier AI, someone in Washington is thinking about how to control it.

How a Handful of Machines Became Geopolitical Leverage

To truly understand export controls explained how a handful of machines became so powerful, you need to appreciate just how concentrated the semiconductor supply chain actually is. Many people assume chip manufacturing is spread across dozens of competitive suppliers. It isn’t. The numbers are staggering.

ASML controls 100% of the EUV lithography market. There is no alternative supplier — period. Every chip manufactured at 7nm or below requires ASML’s machines, and those are the nodes that matter for AI. The company shipped only 53 EUV systems in all of 2023. Each one weighs about 180 tons and requires multiple Boeing 747 cargo flights to deliver. That logistics detail alone reframes the entire policy debate.

TSMC manufactures roughly 90% of the world’s most advanced chips. Taiwan Semiconductor Manufacturing Company, based in Taiwan, is the foundry that builds chips for NVIDIA, Apple, AMD, and dozens of others. Samsung makes some advanced chips too, but nobody else comes close. That geographic concentration — the world’s most critical manufacturing hub sitting 100 miles from mainland China — is something policymakers think about constantly.

Applied Materials, Lam Research, KLA, and Tokyo Electron dominate semiconductor equipment. Together with ASML, these five companies supply nearly all the critical tools needed to build a modern fab. Five companies. That’s the real kicker.

Consequently, controlling just a handful of companies means controlling global AI capability. This is why the “handful of machines” framing isn’t metaphorical — it’s literal. Specifically, about 50–60 EUV lithography systems per year determine who gets to build cutting-edge AI chips. Wrap your head around that number for a second.

Meanwhile, China has poured billions into domestic alternatives. SMIC, China’s leading chipmaker, has reportedly produced some 7nm chips using older deep ultraviolet (DUV) technology. Nevertheless, experts say these efforts face severe yield problems and can’t scale to meet AI training demands. The gap between what China can produce domestically and what’s needed for frontier AI remains enormous — and notably, it widens with every new chip generation.

Similarly, Russia’s semiconductor industry operates at nodes decades behind the cutting edge. Iran has virtually no advanced chip manufacturing capability. The physical constraints of semiconductor manufacturing make catch-up extraordinarily difficult, which is precisely why these controls have teeth.

The Nuclear Analogy: Chips Are the New Centrifuges

The comparison between chip export controls and nuclear non-proliferation isn’t casual. Policymakers have explicitly drawn this parallel, and it comes up repeatedly in policy discussions. When you examine the structural similarities, the analogy holds up remarkably well.

Nuclear weapons require enriched uranium or plutonium. Producing these materials demands specialized centrifuges and reactors. The Nuclear Suppliers Group coordinates export restrictions on these technologies. Similarly, advanced AI requires specialized chips, and producing those chips demands specialized lithography machines. The logic is structurally identical.

Both systems share key characteristics:

- Extreme technical barriers to entry — you can’t build centrifuges or EUV machines in a garage

- Concentrated supply chains — a few companies and countries control critical components

- Dual-use concerns — the same technology enables both civilian and military applications

- Verification challenges — monitoring compliance requires serious intelligence capabilities

- Escalation dynamics — restricted nations pursue workarounds and indigenous alternatives

Although the analogy isn’t perfect, it shows why governments treat these controls so seriously. Export controls explained how a handful of machines became the enforcement mechanism for AI governance isn’t just a policy story. It’s a story about the physical limits of technology transfer — and those limits are more durable than most people assume.

Importantly, chip controls actually outperform nuclear non-proliferation in one specific area. Nuclear material, once acquired, lasts indefinitely — chips don’t. They become obsolete within a few years. A nation cut off from the latest chips falls further behind with every new generation. This depreciation effect makes chip controls uniquely powerful over time. It’s one of the more compelling arguments for the hardware-first approach, and it doesn’t get nearly enough attention in mainstream coverage.

Conversely, chip controls face challenges that nuclear controls don’t. The commercial AI chip market is vastly larger than the nuclear materials market. Thousands of companies need advanced chips for entirely legitimate commercial purposes. Distinguishing between a data center training a language model for customer service and one training a military targeting system is, practically speaking, nearly impossible.

Real-World Impacts and Enforcement Challenges

Understanding export controls explained how a handful of machines became strategic tools requires looking at what’s actually happening on the ground. The impacts are substantial — and so are the problems. Compliance officers at chip companies describe the current environment as unlike anything they’ve seen before.

Impact on China’s AI development. Chinese AI companies like Baidu, Alibaba, and ByteDance have faced real constraints. Training frontier models requires tens of thousands of top-tier GPUs running for months. Without access to NVIDIA’s best chips, Chinese firms reportedly stockpiled older chips before restrictions took effect. Some have turned to cloud computing workarounds, accessing restricted chips through overseas data centers. The restrictions are clearly biting, even if they haven’t stopped progress entirely.

Impact on U.S. companies. NVIDIA has lost billions in potential China revenue. Jensen Huang, the company’s CEO, has publicly warned that overly broad restrictions could push China toward building its own chip ecosystem faster. AMD, Intel, and other chipmakers face similar revenue pressures. The short-term cost to American companies is real — and it’s not nothing.

Smuggling and diversion. Despite controls, restricted chips have shown up in China through third-party countries. BIS has added entities in Singapore, Malaysia, and the UAE to its Entity List for suspected diversion. Enforcement remains a cat-and-mouse game — and the cat doesn’t always win.

The cloud loophole. If a Chinese company can’t buy an H100 GPU, can it rent one from a U.S. cloud provider’s overseas data center? Recent rules now restrict remote access to controlled computing power, not just physical chip transfers. However, enforcement remains technically challenging. This is an area where the rules are moving faster than the technology to enforce them.

Key enforcement mechanisms include:

- End-use monitoring — BIS conducts post-shipment checks

- License requirements — exporters must apply for permits

- Entity List restrictions — specific companies and organizations are blacklisted

- Foreign Direct Product Rule — items made with U.S. technology anywhere in the world can be controlled

- Know Your Customer obligations — exporters must verify buyers aren’t fronts

Nevertheless, the scale of global semiconductor trade makes perfect enforcement impossible. Millions of chips ship worldwide every year, and tracking each one is impractical. Consequently, enforcement focuses on the most impactful chokepoints: the equipment, the highest-performance chips, and the most concerning end users. That’s a reasonable prioritization, but gaps remain.

Additionally, allied coordination remains fragile. Japan and the Netherlands agreed to restrict some equipment exports, but their controls aren’t identical to U.S. rules. Gaps exist. Companies in allied countries sometimes resent losing business to satisfy American strategic priorities — and that resentment, moreover, creates political pressure to loosen controls over time.

What Comes Next: The Future of Hardware-Based AI Governance

The story of export controls explained how a handful of machines became central to AI governance is still being written. Several trends will shape the next chapter.

China’s indigenous chip efforts are accelerating. Huawei’s Ascend 910B processor has emerged as a domestic alternative to NVIDIA chips. It’s not as capable, but it’s improving. China is reportedly spending over $100 billion on semiconductor self-sufficiency. The question isn’t whether China will close the gap — it’s how long it will take. Most analysts think it’s measured in years, not decades.

New chip architectures could complicate controls. Current rules focus on specific performance thresholds measured in TOPS (trillions of operations per second) and interconnect bandwidth. However, novel architectures — neuromorphic chips, photonic computing, analog AI accelerators — might not fit neatly into existing control frameworks. Regulators will need to adapt quickly, and historically that’s not something regulatory bodies do well.

Multilateral frameworks are evolving. The Wassenaar Arrangement, which coordinates export controls among 42 participating states, is increasingly relevant to AI hardware. China isn’t a member, though, and consensus among existing members is difficult to achieve. That structural gap is a real problem.

Compute governance is emerging as a field. Researchers and policymakers are developing new frameworks for governing AI through its computational requirements. This includes proposals for:

- International compute monitoring agreements

- “Know Your Customer” requirements for cloud GPU access

- Compute thresholds that trigger regulatory review

- Hardware-based safety mechanisms built into chips themselves

Importantly, the hardware approach to AI governance holds a fundamental advantage — it’s grounded in physical reality. You can count chips. You can track lithography machines. You can monitor power consumption at data centers. These are tangible, measurable things. Software-based governance, by contrast, struggles with verification at every level. That’s not a minor advantage — it’s the whole reason this approach is worth taking seriously.

Moreover, as AI capabilities advance, the stakes of hardware control will only increase. Today’s frontier models require thousands of advanced GPUs. Tomorrow’s may require millions. The concentration of computing power needed for the most capable AI systems will likely grow, not shrink — which makes the handful of machines at the top of the supply chain even more critical going forward.

Conclusion

When export controls explained how a handful of machines became the new nuclear non-proliferation framework, they revealed something important about AI governance. The most effective control point isn’t code — it’s silicon.

The physical constraints of semiconductor manufacturing create natural chokepoints. A single Dutch company’s lithography machines. A single Taiwanese foundry’s production lines. A handful of equipment makers in the U.S. and Japan. These bottlenecks give governments leverage that no software regulation can match.

Here’s what you should take away:

- Follow the hardware, not the headlines. AI policy debates focus on models, but the real action is in chip controls.

- Understand the tiers. Your country’s tier classification determines what AI hardware you can access — check the BIS website for current classifications.

- Watch for enforcement updates. Rules change frequently. If you work in AI, semiconductors, or cloud computing, compliance awareness is essential. The pace of rule changes has genuinely accelerated since 2022.

- Track China’s progress. The effectiveness of these controls depends heavily on how quickly China builds domestic alternatives.

- Think multilaterally. Unilateral controls leak, and effective governance consequently requires allied coordination.

The story of export controls explained how a handful of machines became geopolitical weapons is ultimately a story about leverage. Right now, a remarkably small number of machines give a remarkably small number of countries an extraordinary amount of it. And if history is any guide, that kind of concentrated leverage doesn’t stay static for long.

FAQ

What exactly are export controls on AI chips?

Export controls on AI chips are government regulations that restrict the sale, transfer, or sharing of advanced semiconductors and chip-making equipment with certain countries or entities. The U.S. Bureau of Industry and Security administers most of these rules. They target specific performance thresholds — notably chips exceeding certain TOPS ratings. These controls cover finished chips, manufacturing equipment, design software, and even technical expertise. It’s a broader net than most people realize.

Why can’t countries just make their own advanced chips?

Building cutting-edge chips requires technology that only a few companies possess. ASML’s EUV lithography machines alone take years to manufacture and cost over $150 million each. Furthermore, operating a modern fab demands thousands of specialized engineers and decades of institutional learning — you can’t hire your way to competence overnight. China is investing heavily in domestic alternatives. However, experts estimate it remains years behind in the most advanced manufacturing processes, and notably that gap compounds with every new generation.

How do chip export controls differ from nuclear non-proliferation?

Both systems target concentrated supply chains and dual-use technologies. However, chips depreciate — they become obsolete within a few years. Nuclear material doesn’t. This makes chip controls uniquely powerful over time, since a country cut off today falls further behind tomorrow. Conversely, the commercial chip market is far larger than the nuclear materials market. Millions of legitimate buyers need advanced chips, and distinguishing military from civilian use is much harder with semiconductors. Neither system is perfect, but they’re structurally more similar than most people appreciate.

Are these export controls actually working?

The evidence is mixed, and anyone who gives you a confident answer either way probably has an agenda. China’s access to the most advanced AI chips has been significantly restricted, and Chinese companies have faced real constraints in training frontier AI models. Nevertheless, smuggling and diversion remain ongoing problems. Additionally, China’s domestic chip industry is making measurable progress, though it still lags considerably. The controls have slowed China’s AI hardware progress but haven’t stopped it entirely. That’s probably the most honest summary available right now.

How do export controls affect regular tech companies and consumers?

Most consumers won’t notice direct effects. However, tech companies operating internationally face significant compliance burdens. Cloud providers must verify that restricted chips aren’t accessed remotely by prohibited entities. AI startups in Tier 2 countries may face limits on how much computing power they can purchase. Importantly, U.S. chip companies like NVIDIA have lost substantial revenue from restricted markets, which could affect their R&D investment over time. That second-order effect doesn’t get discussed enough.

Keep reading

Here are the latest posts from the blog.

Understanding what makes model ‘frontier’ fuzzy line labs use isn’t just about reading press releases. It’s about digging into the evaluation frameworks that actually back th…

Geopolitical AI access: why location matters isn’t just a theoretical concern anymore. It’s a daily reality for millions of researchers, developers, and businesses worldwide…

Table of contents Introduction Why This Matters Step-by-Step Implementation Comparison Table Common Mistakes to Avoid FAQ Conclusion Introduction Choosing between teleoperati…